‘American Families Plan’ Tax Proposal: What You Need to Know

Back in April, the Biden Administration proposed numerous changes to the tax code which underwent various changes in the legislative text and is being debated this week in Congress. The most recent iteration of this proposed legislation released on September 13 does provide some guidance as to what could potentially become law (nothing yet is set in stone). As things stand, the current proposal may impact the financial situation of many individuals. Below are some of the major proposals that could impact you:

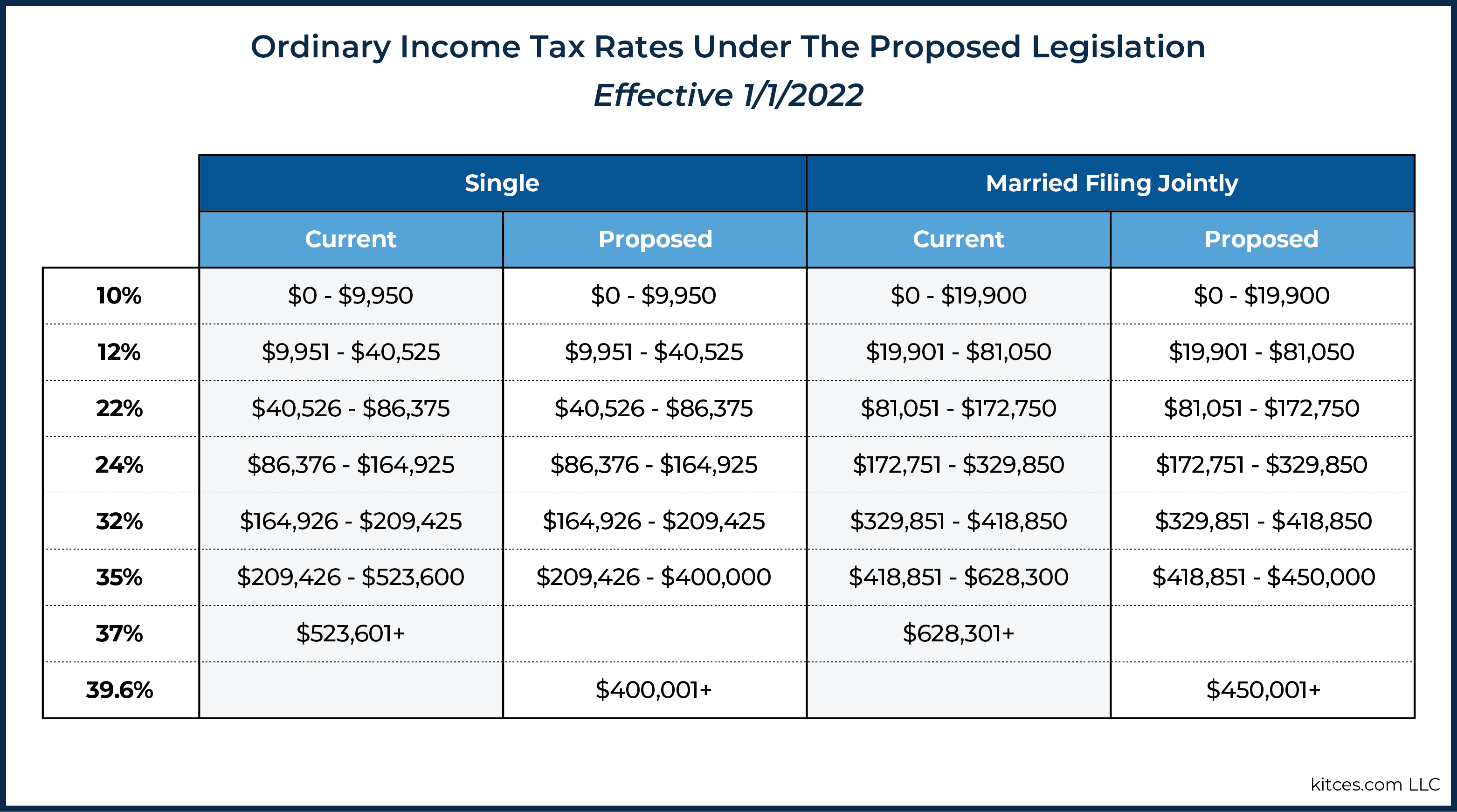

Return of the 39.6% Ordinary Tax Bracket

The Tax Cuts and Jobs Act of 2017 reduced the highest tax bracket to 37%. Under the current proposal, not only would the 39.6% tax bracket return but the income threshold to reach the 39.6% bracket will be drastically reduced. Below is a helpful chart illustrating the new income threshold for each tax bracket:

If these new rates do come to pass, folks who have income about $400k (single)/$450k (joint) should work with the financial advisor to consider ways to accelerate income into 2021.

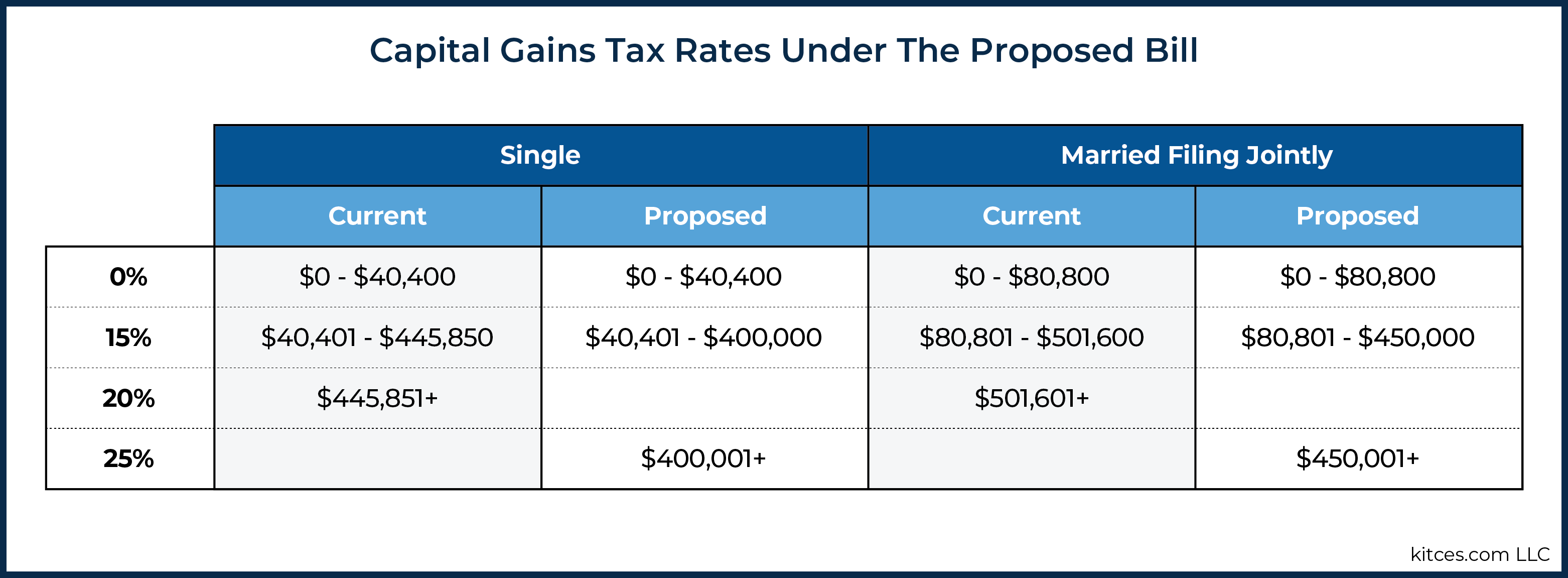

New Long-Term Capital Gains Rate

Along with the proposed increase ordinary income tax rates, there is also another proposal add a 25% tax bracket to the long-term capital gains rate schedule.

Unlike the proposed change to the ordinary income tax rates (which would not be effective until 1/1/2022), this long-term capital gains tax proposal would take effect immediately, should any long-term capital gains be realized on or after 09/14/2021.

Conversions of After-Tax Contributions

Under the latest proposal, the strategies known as the “Backdoor Roth IRA” (i.e. contributing after-tax dollars to a Traditional IRA, then converting the contribution to a Roth IRA) and the “Mega-Backdoor Roth IRA (i.e. contributing after-tax dollars to a 401(k), 403(b), etc. and converting the contribution to a Roth IRA) would unfortunately be prohibited beginning in 2022.

If this provision is passed, those who will be affected by this change should consider the pros and cons making these conversion(s) before the 2021 tax year ends.

New Required Minimum Distributions for Individuals with High Income AND Large Retirement Accounts

A new RMD requirement has been proposed, regardless of age, that may be effective beginning 2022. Upon a closer look, the new RMD is a two-fold requirement:

- High income – A new proposed Adjusted Taxable Income (ATI) threshold of $400,000 for Single filers and $450,000 for Joint filers.

- Retirement Accounts – The total value of your retirement accounts is worth more than $10 million.

If you meet these two criteria, you will be subject to a new type of RMD for the year.

For individuals with retirement account values between $10 million and $20 million, the RMD amount would be equal to 50% of the total retirement account value in excess of $10 million (e.g. If the value of your accounts are $12 million, your RMD would be $1 million).

Special RMD Rules for Roth IRAs

While normally, Roth IRAs are not subject to RMDs, the point above makes an exception to this rule. In order for a Roth IRA to be subject to this special RMD rule, you would need to be a high-income (as defined above) Roth IRA owner AND have a total retirement account value in excess of $20 million.

To make matters more complicated, before completing the 50% RMD in the point above, individuals in excess of the $20 million mark, must complete a separate RMD by distributing the lesser of:

- Total Balances in all Roth accounts (i.e. Roth IRAs or Roth 401(k)s, Roth 403(b), etc.); or

- The amount necessary to reduce the total retirement accounts value to $20 million.

Unified Credit Amount for Estate and Gift Taxes

The TCJA of 2017 increased the estate and gift tax exemption from $5 million to $10 million (with inflation adjustments along the way). While this was always set to revert back to the $5 million mark at the end of 2025, this new proposal seeks to accelerate the timeframe to revert back to the inflation-adjusted $5 million mark starting in 2022.

Assuming this proposed change comes to pass, it may be wise for individuals who will have an estate larger than the $5 million mark to consider some sort of accelerated gifting strategy in order to take advantage of the current exemption level.

Extended Child Tax Credit

In this year alone, the Child Tax Credit underwent a few change (i.e. increasing the credit amount from $2,000 to $3,000, further expanding it to $3,600 for children under age 6, and providing the Credit as an advance monthly payment for eligible families for the second half of 2021.

The new proposal seeks to extend the current Child Tax Credit rules through 2025. The currently advance monthly payments are extended through 2022. However, beginning in 2023, the Child Tax Credit is formally transitioning into a monthly credit of $250/month/child (for children age 6+) and $300/month/child (for children under age 6).

Conclusion

Many changes could be taking place relatively quickly and it is still too soon to tell what may or may not actually pass as law. Should the proposal mentioned above come to pass, it is highly recommended that you consult with a fee-only financial advisor if you are impacted. Your financial goals may have to be re-examined to accommodate these sweeping changes.

Weingarten Associates is an independent, fee-only Registered Investment Advisor in Lawrenceville, New Jersey serving Princeton, NJ as well as the Greater Mercer County/Bucks County region. We make a difference in the lives of our clients by providing them with exceptional financial planning, investment management, and tax advice.